Markets brace for hot consumer inflation report in the week ahead

9월 10일 20213:46 EDTupdated FRI, 9월 10일 20214:38 EDT

PUBLISHED FRI, SEP 10 20213:46 PM EDT UPDATED FRI, SEP 10 20214:38 PM EDT

by Patti Domm@IN/PATTI-DOMM-9224884/@PATTIDOMM

The translation

만약 CPI(소비자 물가 지수; Consumer Price Index)가 예상보다 더 뜨거울 경우, 전략가들은 연준위가 조만간 채권 매입을 축소하는 것을 고려하도록 움직이는 촉매제가 될 수 있다고 말한다.

주요 소매 판매 보고서도 있는데, 이것은 소비의 둔화를 보여줄 것으로 예상되며, 그것은 인플레이션이 회복되는 동안 경기 침체의 두 가지 위협에 대한 더 많은 우려를 촉발시킬 수 있다.

투자자들은 요즘 인플레이션에 대한 어떤 수치에도 촉각을 곤두세우고 있고 소비자 물가 지수는 다음 주에 가장 큰 관심사가 될 것이다.

가장 최근의 경제 상황은 연방준비제도 이사회가 중요한 9월 회의를 불과 일주일 앞두고 나온 것이다. 이번 회의에서 연준은 채권 매입 프로그램 또는 양적 완화를 축소하려는 계획에 대해 보다 자세한 내용을 논의할 것으로 예상된다.

시장 전문가들은 인플레이션 지수가 높아지면 매달 1200억 달러의 채권 매입을 늦추려는 연방준비제도 이사회(FRB)의 계획을 앞당길 수 있다고 말한다. 자산 매입 프로그램의 축소는 연방준비제도 이사회가 전염병과 싸우기 위해 시행한 쉬운 정책에서 벗어나는 첫 번째 주요 조치가 될 것이다.

소비자물가지수는 화요일로 예상되며 소매 판매 데이터는 목요일에 발표된다. FactSet의 컨센서스 추정에 따르면, 8월 소비자물가가 연 5.3%의 속도로 뛰어올랐으며, 소비자는 연초 높은 소비 수준에서 계속 후퇴할 것으로 예상된다.

뜨거운 소비자물가지수(Hot CPI)

"만약 CPI가 예상보다 더 뜨겁다면, 9월에 발표될 테이퍼링과 11월을 기다리는 것 사이에 차이를 만들 수 있을 것입니다,"라고 스털링 자문 그룹의 최고 투자 책임자인 피터 부크바씨는 말했다.

경제학자들은 CPI가 매월 0.4%의 속도로 상승할 것으로 예상하고 있다. 이 보고서는 금요일에 발표된 8월 생산자물가지수가 공급망 제약으로 인해 매년 8.3%씩 상승한 데 따른 것이다.

소비자 물가 지수, 1년 전과 백분율 변화

미국 도시 평균의 모든 항목

연방준비제도이사회(FRB)가 11월이나 12월에 채권 매입 프로그램(QE) 완화에 대한 공식 발표를 할 것으로 예상되고 있다. 9월 발표를 예상했던 많은 사람들은 8월 고용보고서가 발표된 이후 예상보다 50만 명 정도 적은 23만 5천 명의 일자리가 늘어난 것으로 나타났다.

"물론 물가상승률이 예상을 상회하는 추세입니다. 만약 그런 일이 다시 일어난다면, 그것은 높은 인플레이션이 고착될 것이라는 이야기를 부채질할 것이라고 생각합니다. 데이비드 도나베디안 CIBC 최고 투자책임자(CEO)는 "채권시장이 QE 테이퍼링 시기를 앞당기거나 1차 금리인상 시기를 앞당기는 것으로 본다면 분명 문제가 될 것"이라고 말했다.

그것은 주식에 마이너스일 것이다.

도나베디안은 연방준비제도이사회(FRB)의 연준 발표와 관련, "만약 시장이 인플레이션 폭동을 일으키고 그 결과 변동성이 생긴다면, 그들은 9월로 이를 앞당길 수 있다"라고 말했다. "하지만 제 생각에는 4분의 1 정도의 가능성이 있는 것 같아요."

스태그플레이션?

인플레이션 증가와 소비 둔화의 조합, 특히 8월의 부진한 일자리 발표 이후 스태그플레이션의 위협에 대한 논의를 촉발시켰다. 경제학자들이 3/4분기 성장률 전망치를 6% 이상에서 5% 조금 넘는 높은 수준으로 하향 조정함에 따라 이러한 우려는 더욱 커졌다.

"저는 '스태그'보다는 '플레이션' 쪽에 더 가깝습니다. 저는 경제가 내년까지 잘 될 것이라고 생각합니다,"라고 도나베디언은 말했다. 그는 올해 초 경기 부양책이 소매 판매를 증가시킨 후 소비지출의 둔화는 놀라운 일이 아니며 단지 "단기 경고"일뿐이라고 말했다.

"우리는 경기 부양금 지급과 백신 접종과 소비자 낙관론의 폭발적 결과로 올해 초에 소매 판매가 폭발적으로 증가했습니다. 이제 정말 안정됐어요,"라고 그는 말했다. "엄청난 유동성과 저축이 있었고, 그들은 여분의 저축액 중에서 그들이 쓴 돈을 썼고, 여러분은 여기서 약간의 후퇴를 겪게 될 것이고, 이것이 경제학자들이 그들의 3/4분기 예상치를 낮추는 이유이다. 소비자 펀더멘털은 상당히 양호합니다."

바클레이스의 수석 경제학자 마이클 게이펜은 연준의 말처럼 CPI 보고서가 인플레이션이 최고조에 달하고 있다는 것을 보여줄 것으로 기대한다고 말했다. 그러나 그는 둔화 추세가 소비지출만의 문제가 아니라고 말한다. 그것은 또한 사업 지출과 주택 분야에서도 나타나고 있다.

"노동시장이 있는 한, 8월은 약간 알맹이였습니다. 하지만 고용 성장은 평균적으로 견실하고, 올해 내내 매우 견실했습니다, "라고 그는 말했다. "8월에 고용이 실망했지만, 시간과 수입은 여전히 꽤 괜찮았습니다. 소비자들에게는 수입이 있습니다. 우리는 이것을 단기적인 딸꾹질로 보고 있습니다."

가펜 연구원은 3분기 경제성장률이 예상보다 다소 둔화될 수 있다고 말했다. 그러나 그는 일부 하락한 성장세가 4분기에 나타날 수 있다고 말했다.

"스태그플레이션의 특징도 있지만 진정한 스태그플레이션은 실업률과 물가 상승이다. 우리는 그것을 가지고 있지 않아요, "라고 그는 말했다. "이런 병목현상은 경기 회복 속도를 억제하고 인플레이션을 높이는 요인이 됩니다. 지금은 수요가 문제가 아닙니다. 공급은. 실업률은 여전히 낮아지고 있고 고용은 개선되고 있다. 냄새는 나지만 스태그플레이션이라고 할 수는 없다고 말했다.

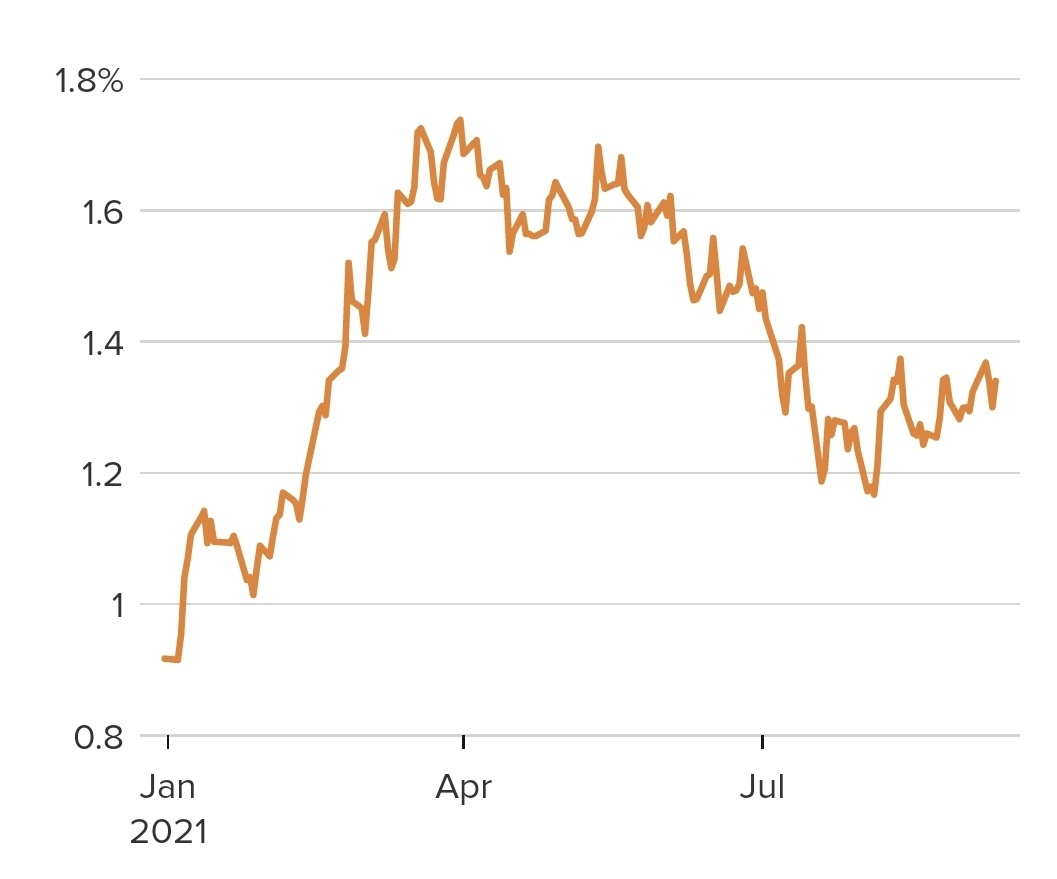

미국 10년 만기 재무부 수익률

도나베디안은 공급망이 계속 차질을 빚고 있기 때문에 내년까지 가격 인상과 부족 현상이 지속될 것으로 예상하고 있다. PPG와 General Electric을 포함한 일부 회사들은 이미 2022년까지의 공급 문제를 어떻게 보고 있는지에 대해 언급했다. 도나베디안은 3/4분기 실적 시즌을 앞두고 더 많은 경고를 받을 것으로 예상하고 있다.

이번 주 S&P 500 지수는 1.7% 하락한 4,458을 기록했다. 주의 깊게 관찰된 10년 만기 재무부 수익률은 1.33%를 상회했고 금요일에는 1.33%였다.

많은 전략가들은 주식 시장이 전형적으로 급등했던 9월과 10월에 후퇴할 것으로 예상하고 있다. 일부에서는 특히 중앙은행이 특히 강경하게 들릴 경우 연준의 9월 회의가 촉매제가 될 수 있다고 말한다.

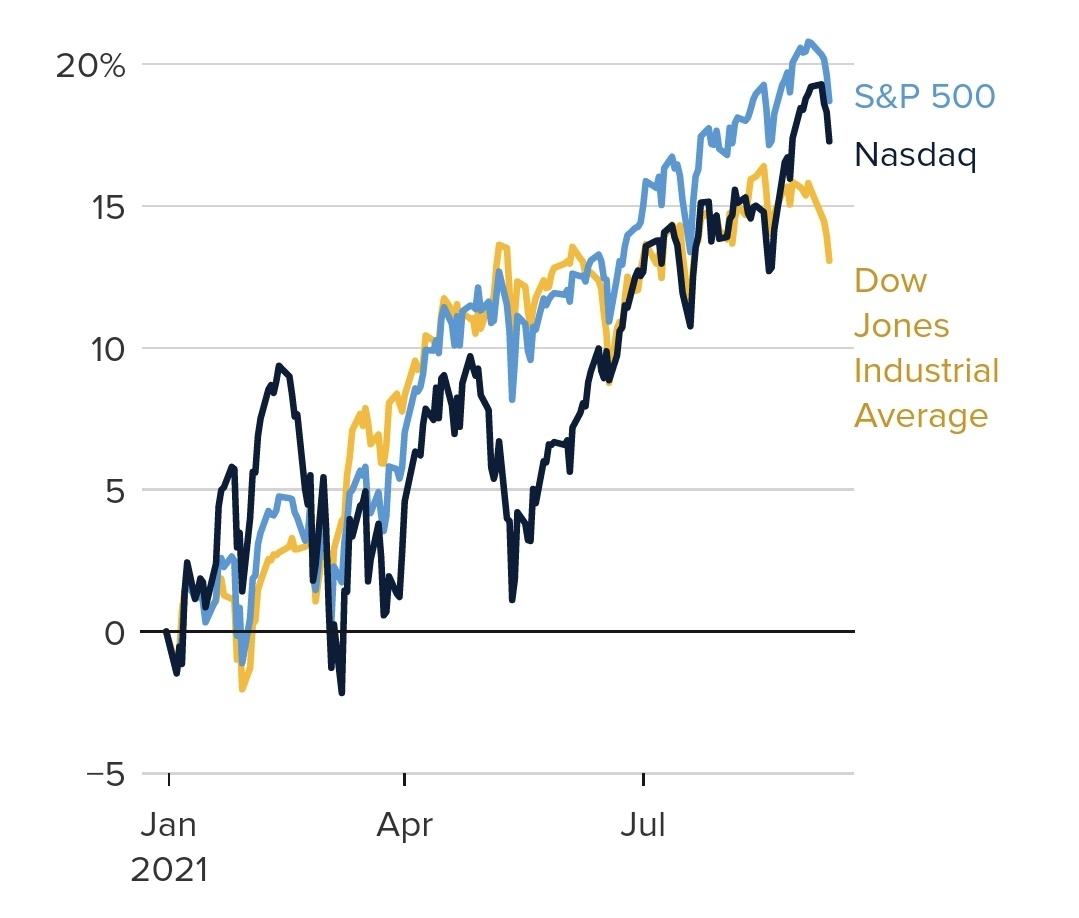

연도별 수익률

"우리는 2019년에 30% 이상, 작년에는 18% 이상, 올해 첫 달에는 21% 이상 상승했습니다,"라고 도나베디안은 말했다. "이는 지속 불가능한 비율이나 수익률입니다. 우리의 중요한 점은 여기서부터 더 어려워질 것이라는 것입니다. 가치는 어느 정도 확장되었고, 이 믿을 수 없을 정도로 지지적인 정책 프레임워크는 조금 덜 우호적이 될 것입니다."

이제 국회를 지켜보자

도나베디안은 사회기반시설 지출과 그에 대한 세금 인상안을 구체적으로 제시하기 시작함에 따라 의회에서 논의되는 것을 지켜보는 것이 중요하다고 말했다.

"그들은 돈이 어디에 사용될 것인지, 그리고 어떤 세금과 세율이 법안에 쓰여질 것인지에 대한 빈칸을 채우기 시작할 것입니다, "라고 그는 말했다. 전체 법인세율, 외국인 근로소득세율, 양도소득세율, 배당세율입니다. 이는 투자와 관련된 큰 이슈라고 말했다.

그는 시장이 세금 문제를 무시해 왔다고 말했다. "이런 종류의 문제들은 여름 동안 잠잠해졌지만, 다음 2주 동안 완전히 지루해졌습니다. 많은 관심을 받을 것입니다."

세금 결정은 주식 시장 수익의 큰 원동력이었던 기업 수익에 큰 영향을 미칠 수 있다. "잘못될 수 있는 가장 직접적인 방법 중 하나는 2022년부터 시행되는 대규모 세금 인상이다. 그것은 직접 머리를 깎은 것입니다, "라고 그는 말했습니다.

다음 주 달력

월요일

수입: 오라클

오후 2시. 연방예산계산서

화요일

오전 6시 NFIB 소형 버스 신덱스

오전 8시 30분 CPI

수요일

오전 7시 30분. 주간 주택담보대출 신청서

오전 8시 30분. 수입가격

오전 8시 30분. 엠파이어 스테이트 제조

오전 9시 15분. 산업생산

목요일

오전 8시 30분. 실업수당 청구

오전 8시 30분. 필라델피아 연방 조사

오전 8시 30분. 소매판매

오후 4시. TIC 데이터

금요일

오전 10시에요. 소비심리

The Original

If the CPI(Consumer Price Index) is hotter than expected, strategists say it could be a catalyst to move the Fed to consider tapering back its bond purchases sooner rather than later.

There is also a key retail sales report, which is expected to show a slowdown in spending, and that could trigger more worries about the twin threats of a slower economy while inflation picks up.

Investors are paying close attention to any reading on inflation these days, and the consumer price index will be the big one to watch in the coming week.

The latest snapshot of the economy comes just a week before the Federal Reserve’s important September meeting.

At that meeting, the Fed is expected to discuss more details about its plan to taper down its bond buying program, or quantitative easing.

Market professionals say a hotter inflation reading could speed up the Fed’s plans to slow the $120 billion a month in bond purchases. The paring back of its asset purchase program would be the Fed’s first major step away from the easy policy it put in place to combat the pandemic.

The consumer price index is expected Tuesday, and there is retail sales data is released Thursday. They are expected to show consumer prices jumped at a 5.3% annual pace in August, according to the consensus estimate from FactSet, while the consumer continued to pull back from the high spending levels of earlier in the year.

Hot CPI

“If the CPI is hotter than expected, it could make the difference between a September announcement for tapering or waiting to November,” Bleakley Advisory Group chief investment officer Peter Boockvar said.

Economists expect CPI to rise at a 0.4% pace month over month. The report comes after August’s producer price index — which was released Friday — showed a jump of 8.3% year over year, due in part to supply chain constraints.

Consumer price index, percent change from a year ago

All items in U.S. city average

The Fed’s formal announcement about tapering its bond-buying program, also called QE, is widely expected in November or December. Many of those who had expected a September announcement pushed back their time frame to later in the year after August’s employment report showed just 235,000 jobs added, about 500,000 less than expected.

“Certainly the trend has been for the inflation number to come in above expectations. I think if that happens again, it will feed the narrative that high inflation is going to stick. Obviously, it’s an issue for the bond market if it’s viewed at all as accelerating the timing of the QE tapering, and or accelerating the timing of the first rate hike,” CIBC Private Wealth U.S. chief investment officer David Donabedian said. That would be a negative for stocks.

“If markets have an inflation mutiny here and there’s volatility as a result, they could move it up to September,” Donabedian said of the Fed’s taper announcement. “But I think there’s kind of a one in four likelihood in my view.”

Stagflation?

That combination of higher inflation and slower spending, particularly after August’s weaker jobs report, has spurred talk about the threat of stagflation. Those worries have also increased as economists ratchet back growth forecasts for the third quarter to a still high level just above 5%, from above 6%.

“I’m more about the ‘flation’ side of it than the ‘stag.’ I think the economy is going to perform fine right through next year,” Donabedian said. He said the slowdown in consumer spending after stimulus checks had boosted retail sales earlier in the year is not surprising and may be just a “short-term warning.”

“We had this explosive growth in retail sales early in the year as a direct result of stimulus payments and vaccines coming and a burst of consumer optimism. It’s really settled down now,” he said. “There was an enormous amount of liquidity and saving and they spent what they spent out of that extra amount of savings and you’re going through a bit of a retracement here, which is why you’re seeing economists mark down their third quarter estimates. Consumer fundamentals are pretty good.”

Barclays chief U.S. economist Michael Gapen said he expects the CPI report to show that inflation is peaking, just as the Fed has said. But he says the slowing trend is not just an issue for consumer spending. It is also showing up in business spending and housing.

“With where labor markets are, August was a bit of an egg. But growth in employment has been solid on average, very robust over the course of the year,” he said. “Even though employment disappointed in August, hours and and earnings were still pretty good. There’s income there for consumers to spend. We’re looking at this as a short-term hiccup.”

Gapen said third-quarter economic growth may be somewhat slower than expected. However, he said some of the lost growth could show up in the fourth quarter.

“It has some characteristics of stagflation, but true stagflation is rising unemployment and rising inflation. We don’t have that,” he said. “These are bottlenecks that are kind of constraining the pace of the recovery and lead to higher inflation. Demand isn’t the problem right now. Supply is. The unemployment rate is still coming down and employment is improving. It has the whiff but I wouldn’t call it stagflation.”

U.S. 10-year Treasury yield

Donabedian expects higher prices and shortages to continue into next year, as supply chains keep getting disrupted.

Some companies, including PPG and General Electric, have already commented on how they see issues with supplies stretching into 2022. Donabedian expects to see more warnings ahead of the third-quarter earnings season.

Stocks were lower this week, with the S&P 500 losing 1.7% to 4,458. The closely watched 10-year Treasury yield has held above 1.3% and was at 1.33% on Friday.

A number of strategists expect to see the stock market pullback during the typically choppy September and October

period. Some say the Fed’s September meeting could be a catalyst, especially if the central bank sounds particularly hawkish.

Year-to-date returns

“We’re up over 30% in 2019, over 18% last year and over 21% in the first months of this year,” Donabedian said. “These are unsustainable rates or return.... Our takeaway is it’s going to get tougher from here. Valuations are somewhat extended and this whole incredibly supportive policy framework is going to get a little less friendly.”

Now watch Congress

Donabedian said it will be important to watch discussions in Congress as it begins to put details around the infrastructure spending and what type of tax increases will be proposed to pay for it.

“They’re going to start to fill in the blanks on where the money is going to be spent and what taxes and tax rates are going to be written into the legislation,” he said. “It’s the overall corporate tax rate, it’s the tax on foreign earned income, capital gains rates and dividend tax rate. These are big investor related issues.”

He said the market has been ignoring the tax issue. “Those sort of issues went quiet over the summer but it’s back full bore over the next two weeks. It will get a lot of attention.”

The tax decisions could have big implications for corporate earnings, which have been a big driver of the stock market’s gains. “One very direct way that could go wrong is if you get a large set of tax increases that go into effect in 2022. That’s a direct hair cut,” he said.

Week ahead calendar

Monday

Earnings: Oracle

2:00 p.m. Federal budget statement

Tuesday

6:00 a.m. NFIB small busines sindex

8:30 a.m. CPI

Wednesday

7:30 a.m. Weekly mortgage applications

8:30 a.m. Import prices

8:30 a.m. Empire State manufacturing

9:15 a.m. Industrial production

Thursday

8:30 a.m. Jobless claims

8:30 a.m. Philadelphia Fed survey

8:30 a.m. Retail sales

4:00 p.m. TIC data

Friday

10:00 a.m. Consumer sentiment

'움직이는 경제' 카테고리의 다른 글

| 다우, 5일 연속 하락 후 200포인트 반등 (0) | 2021.09.14 |

|---|---|

| 다우, S&P 500 공포? 수정에 대해 걱정하는 것이 여전히 잘못된 투자 방법인 이유 (0) | 2021.09.13 |

| 다우, 5일 연속 하락, 200포인트 반등 (0) | 2021.09.11 |

| 직원을 위한 COVID 백신이 필요한 미국 기업 (0) | 2021.09.10 |

| 다우지수, S&P 나흘째 적자를 기록한 후 주식 선물은 개장 반등세로 돌아섰다 (0) | 2021.09.10 |

댓글